Deep Learning Increases the Oil Production by 30% While Reducing CAPEX

Our Measurable Values

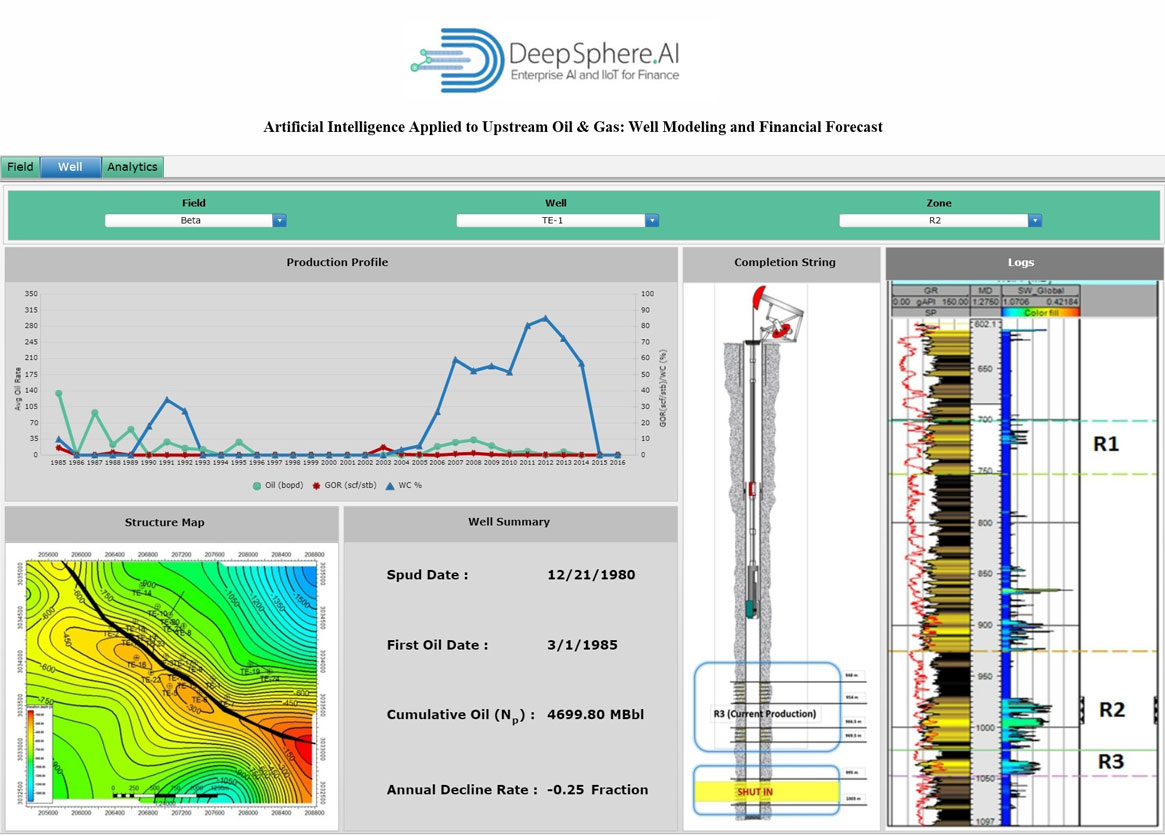

The term “Oil Rate” is defined as means of measuring how many barrels of oil a day a oil well produces. The initial Oil production rate is important because it is used to extrapolate a well’s total production, its peak production level and the rate at which production will decline using a decline- curve analysis. Oil wells typically have an initial production rate that is fairly small compared to peak production because oil production follows a bell curve. However, shale oil wells decline much more rapidly after the initial surge. Production can fall to 50-85% of the IP rate within a year, and to less than 10% of their IP rate after three years.

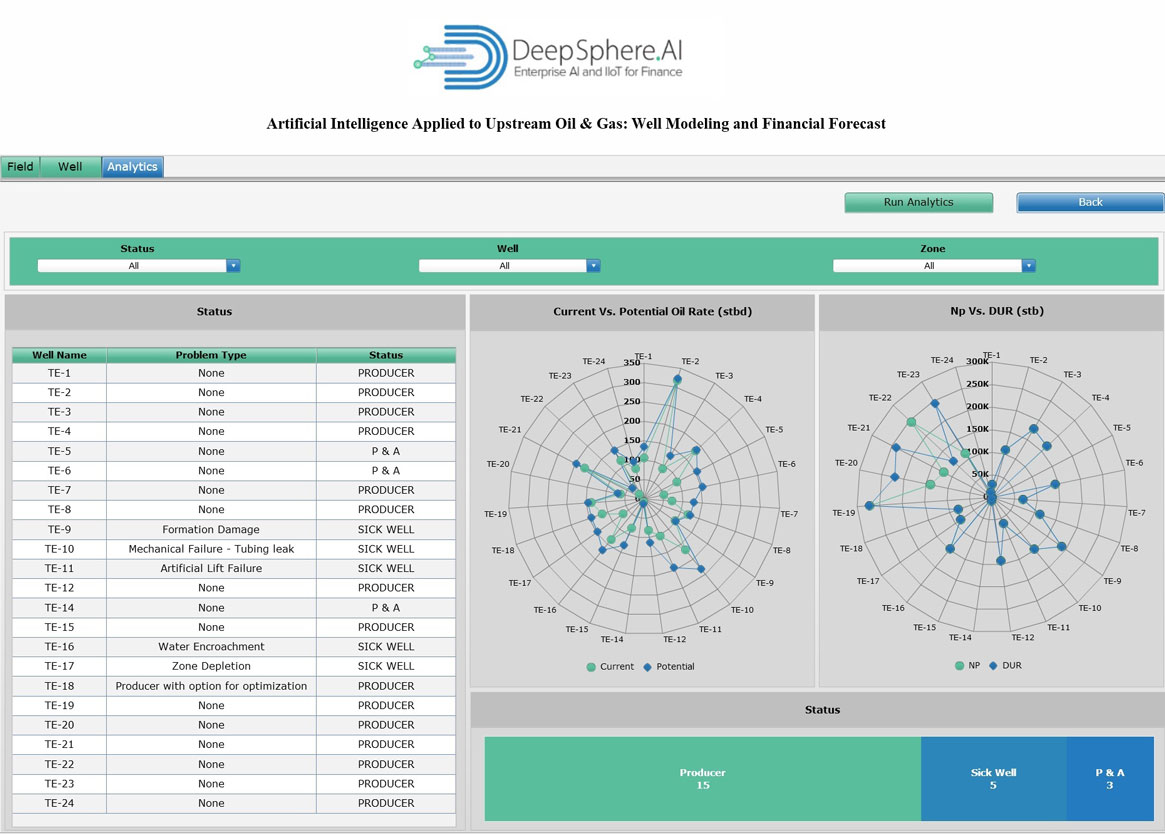

The production of oil or gas from underground reservoirs involves chemical and mechanical processes that affect the wellbore. Many of these processes can eventually cause a problem with the well, resulting either in a decrease in production or in failure of equipment installed downhole or at the surface. Most of the serious problems can be avoided or delayed through preventive maintenance techniques or early recognition from regular analysis of producing rates, fluids, and the mechanical condition of the well. Such practices can prevent a costly workover that may be required to restore production from the well and may also prevent total loss of the wellbore.

The term “Water Cut” is defined as the ratio of water produced compared to the volume of total liquids produced. The water cut in water drive reservoirs can reach very high values. A well that makes 50 barrels of oil per day and 150 barrels of water a day has a water cut of 150/(50+150) = 75%. Water cuts in producing wells typically increase as oil fields mature with estimated water disposal cost of about $40 billion worldwide.

Managing water production is often the key to optimizing oil production. Water drive provides the driving energy of many oil reservoirs, so water production is inevitable, and a good thing in a way. But water provides no revenue, and actually costs money to separate and dispose. At the point where total costs, including the cost of handling water, exceeds the net revenue from production, the operator is losing money.

Water cut for crude oil flowing in a pipeline can be measured using water-cut meters. Water-cut meters are typically used in the mineral oil industry to measure the water content in oil flowing from a well, produced oil from a separator, crude oil transfer in pipelines and in loading tankers. There are several technologies used. The main technologies are dielectric measurements using radio or microwave frequency.

“Cumulative Oil” is defined as the gross amount of oil production from an oil reservoir over a particular period of time of the life of a well. In general, cumulative production is an Oil and Gas industry term related to an oil well, a basin or an oil field. Cumulative production of oil can be calculated by multiplying the amount of production by the rate. The data gathered from the cumulative production and production rate of an Oil and Gas reservoir is analyzed to keep track of the productive oil wells over a time period, for example a year.

An energy producer extracts oil from a well as long as the field is producing enough amount of Oil and Gas. The company conducts a survey on the field, basin or the well to determine how much Oil and Gas has been produced from it over a specific time span. The gross total of Oil and Gas produced is known as cumulative production, which is calculated by multiplying the rate with the amount of production. Ideally, the cumulative production of all oil reservoirs is calculated annually.

“Cumulative Water” is defined as the gross amount of water production from an oil reservoir over a particular period of time of the life of a well. In general, cumulative production is an Oil and Gas industry term related to an oil well, a basin or an oil field. Cumulative production of water can be calculated by multiplying the amount of production by the rate. The data gathered from the cumulative production and production rate of an Oil and Gas reservoir is analyzed to keep track of the productive oil wells over a time period, for example a year.

An energy producer extracts oil from a well as long as the field is producing enough amount of Oil and Gas. The company conducts a survey on the field, basin or the well to determine how much Oil and Gas has been produced from it over a specific time span. The gross total of Oil and Gas produced is known as cumulative production, which is calculated by multiplying the rate with the amount of production. Ideally, the cumulative production of all oil reservoirs is calculated annually.

“Cumulative Gas” is defined as the gross amount of gas production from an oil reservoir over a particular period of time of the life of a well. In general, cumulative production is an Oil and Gas industry term related to an oil well, a basin or an oil field. Cumulative production of gas can be calculated by multiplying the amount of production by the rate. The data gathered from the cumulative production and production rate of an Oil and Gas reservoir is analyzed to keep track of the productive oil wells over a time period, for example a year.

An energy producer extracts oil from a well as long as the field is producing enough amount of Oil and Gas. The company conducts a survey on the field, basin or the well to determine how much Oil and Gas has been produced from it over a specific time span. The gross total of Oil and Gas produced is known as cumulative production, which is calculated by multiplying the rate with the amount of production. Ideally, the cumulative production of all oil reservoirs is calculated annually.

When oil is brought to surface conditions it is usual for some natural gas to come out of solution. The “Gas/Oil Ratio” (GOR) is the ratio of the volume of gas that comes out of solution, to the volume of oil at standard conditions. The Gas/Oil Ratio (GOR) is a dimensionless ratio (volume per volume) in metric units, but in field units, it is usually measured in cubic feet of gas per barrel of oil or condensate. Gas/Oil ratio (GOR) is a measurement typically displayed along with other basic well metadata. It is a determining factor in whether the well is classified as a gas or oil well (as its primary hydrocarbon product).

It is common that both gas and oil will be produced from the same well. For any hydrocarbon mixture produced from an oil production well, the proportion of liquid and vapor phases in the mixture changes with changing temperature and pressure conditions. In order to compare the Gas/Oil Ratio (GOR) from different Oil and Gas samples, the Oil and Gas flow rates must be considered at same temperature and pressure conditions.

Hence the Gas/Oil Ratio (GOR) is always specified at standard temperature and pressure conditions. The liquid and vapor volumetric flow rates are calculated at standard temperature and pressure conditions, expressed in sm3/hr. Sometimes only the gas volume is expressed at standard conditions and liquid volume is expressed in barrels. Then the Gas/Oil Ratio (GOR) is expressed in sm3/bbl.

“Current Oil Rate” is defined as the Rate at which the oil well is producing currently. Oil production is the quantities of oil extracted from the ground after the removal of inert matter or impurities. It includes crude oil, natural gas liquids (NGLs) and additives. This indicator is measured in athousand ton of oil equivalent (toe).Crude oil is a mineral oil consisting of a mixture of hydrocarbons of natural origin, yellow to black in colour, and of variable density and viscosity.

NGLs are the liquid or liquefied hydrocarbons produced in the manufacture, purification and stabilisation of natural gas. Additives are non-hydrocarbon substances added to or blended with a product to modify its properties, for example, to improve its combustion characteristics (e.g. MTBE and tetraethyl lead). Refinery production refers to the output of secondary oil products from an oil refinery.

“Potential Oil” Rate is defined as the rate at which the oil well has the maximum capacity of producing oil in the future. Oil production is the quantities of oil extracted from the ground after the removal of inert matter or impurities. It includes crude oil, natural gas liquids (NGLs) and additives. This indicator is measured in thousand ton of oil equivalent (toe). Crude oil is a mineral oil consisting of a mixture of hydrocarbons of natural origin, yellow to black in colour, and of variable density and viscosity.

NGLs are the liquid or liquefied hydrocarbons produced in the manufacture, purification and stabilisation of natural gas. Additives are non-hydrocarbon substances added to or blended with a product to modify its properties, for example, to improve its combustion characteristics (e.g. MTBE and tetraethyl lead). Refinery production refers to the output of secondary oil products from an oil refinery.

“Net Production” (Np) is defined as amount of oil and/or gas a well generates that is owned and available for distribution after taxes, royalties, expenses are paid. Oil production is the quantities of oil extracted from the ground after the removal of inert matter or impurities. It includes crude oil, natural gas liquids (NGLs) and additives. This indicator is measured in thousand ton of oil equivalent (toe).Crude oil is a mineral oil consisting of a mixture of hydrocarbons of natural origin, yellow to black in colour, and of variable density and viscosity.

NGLs are the liquid or liquefied hydrocarbons produced in the manufacture, purification and stabilisation of natural gas. Additives are non-hydrocarbon substances added to or blended with a product to modify its properties, for example, to improve its combustion characteristics (e.g. MTBE and tetraethyl lead). Refinery production refers to the output of secondary oil products from an oil refinery.

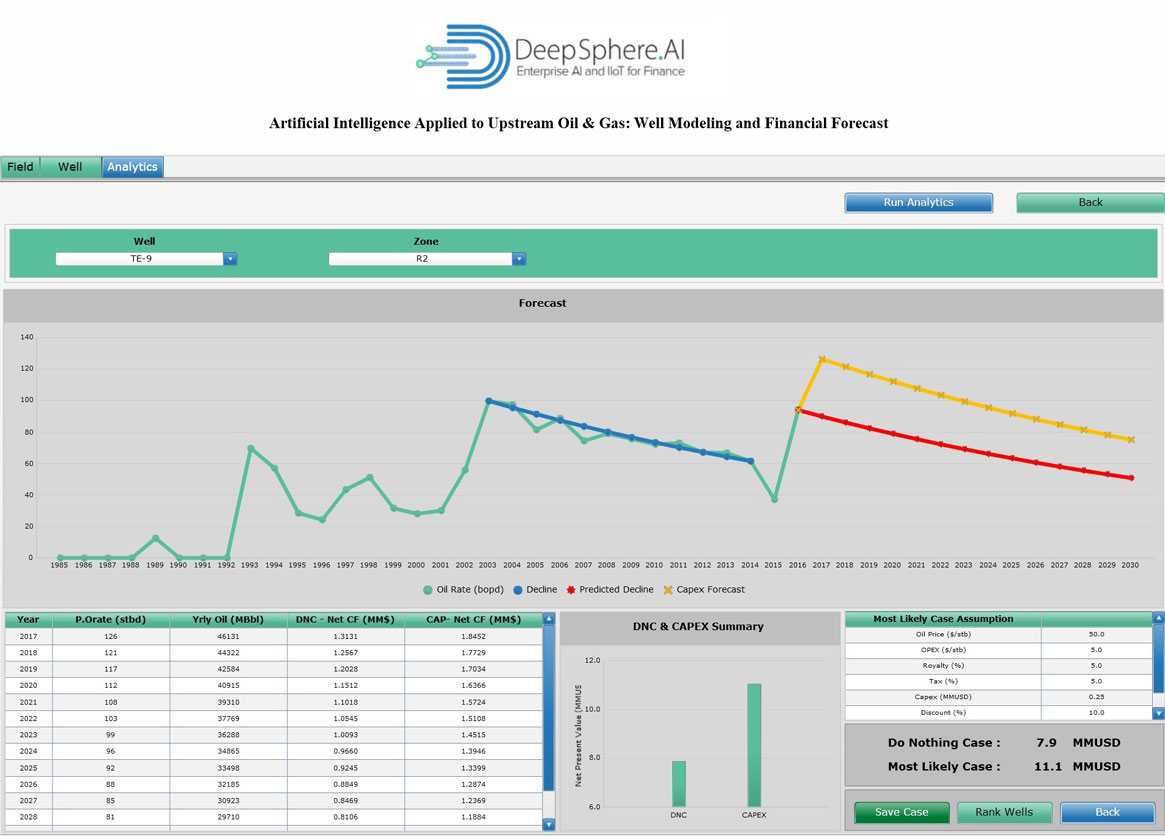

Ultimate Recovery, also known as “Discovered Ultimate Recovery (DUR)”, is the total ultimate discovered recovery of oil or gas from a reservoir rock by the end of its producing life. These estimated recoverable values from a reservoir are generally approximate values derived from various mathematical models and units depending on the study being conducted. E&P organizations must factor ultimate recovery in order for the production project to be viable and profitable.

The Ultimate Recovery or Discovered Ultimate Recovery (DUR) value represents the rough possible quantity of hydrocarbons recoverable from an oil well. These values help decision makers to decide whether the project would be economically viable or not for the E&P organization. Thus, based on the DUR figures and certain other parameters, the organization can decide whether they should invest into the development of an oil or gas well on a particular hydrocarbon reservoir on which studies are being conducted.

During project execution phase in the Oil and Gas E&P business, one important parameter check needs to be performed, i.e., the drilling project should meet an acceptable discovered ultimate recovery (DUR) threshold value in order for the well drilling to proceed.

The term “Decline Rate” is the rate at which the production is declining. Decline Rate refers to the annual reduction in the rate of production from an individual field or a group of fields, after a peak in production. Detailed empirical analyses of decline rates have been produced for well over 50 years and most studies tend to agree on the typical decline rates for different categories of field, despite some differences in details.

Decline curve analysis (DCA) is a graphical procedure used for analyzing declining production rates and forecasting future performance of Oil and Gas wells. Oil and gas production rates decline as a function of time; loss of reservoir pressure, or changing relative volumes of the produced fluids, are usually the cause. Fitting a line through the performance history and assuming this same trend will continue in future forms the basis of DCA concept. It is important to note here that in absence of stabilized production trends the technique cannot be expected to give reliable results.

The decline curve is a method for estimating reserves and predicting the rate of oil or gas production. It typically shows the pace at which production is expected to decline over the lifetime of an energy asset. Knowing the decline curve can help a producer estimate the quantity of oil reserves that can come from a well over its lifetime, the present and future value of a well, and the rate at which assets should depreciate on a company’s books. In aggregate, the decline curve can also help determine the rate of production for a total reservoir or even multiple reservoirs.

The term Oil and Gas “Capital Expenditure, or CAPEX,”is financing used by companies to secure physical assets or upgrade current assets. CAPEX generally takes two forms; maintenance expenditure, in which a company purchases assets that extend the useful life of existing assets, and expansion expenditure, in which a company purchases new assets in an effort to grow the business.

CAPEX is basically capital expenditures such as drilling & completing a well. It’s a critical component to capital budgeting and should be monitored well. Capital Expenditures incurred in exploration activities should be expensed unless they meet the definition of an asset. An entity recognizes an asset when it is probable that economic benefits will flow to the entity as a result of the expenditure. The economic benefits might be available through commercial exploitation of hydrocarbon reserves or sales of exploration findings or further development rights. It is difficult for an entity to demonstrate that the recovery of exploration expenditure is probable. Where entities do not adopt IFRS 6 and instead develop a policy under the Framework, expenditures on an exploration property are expensed until the capitalization point.

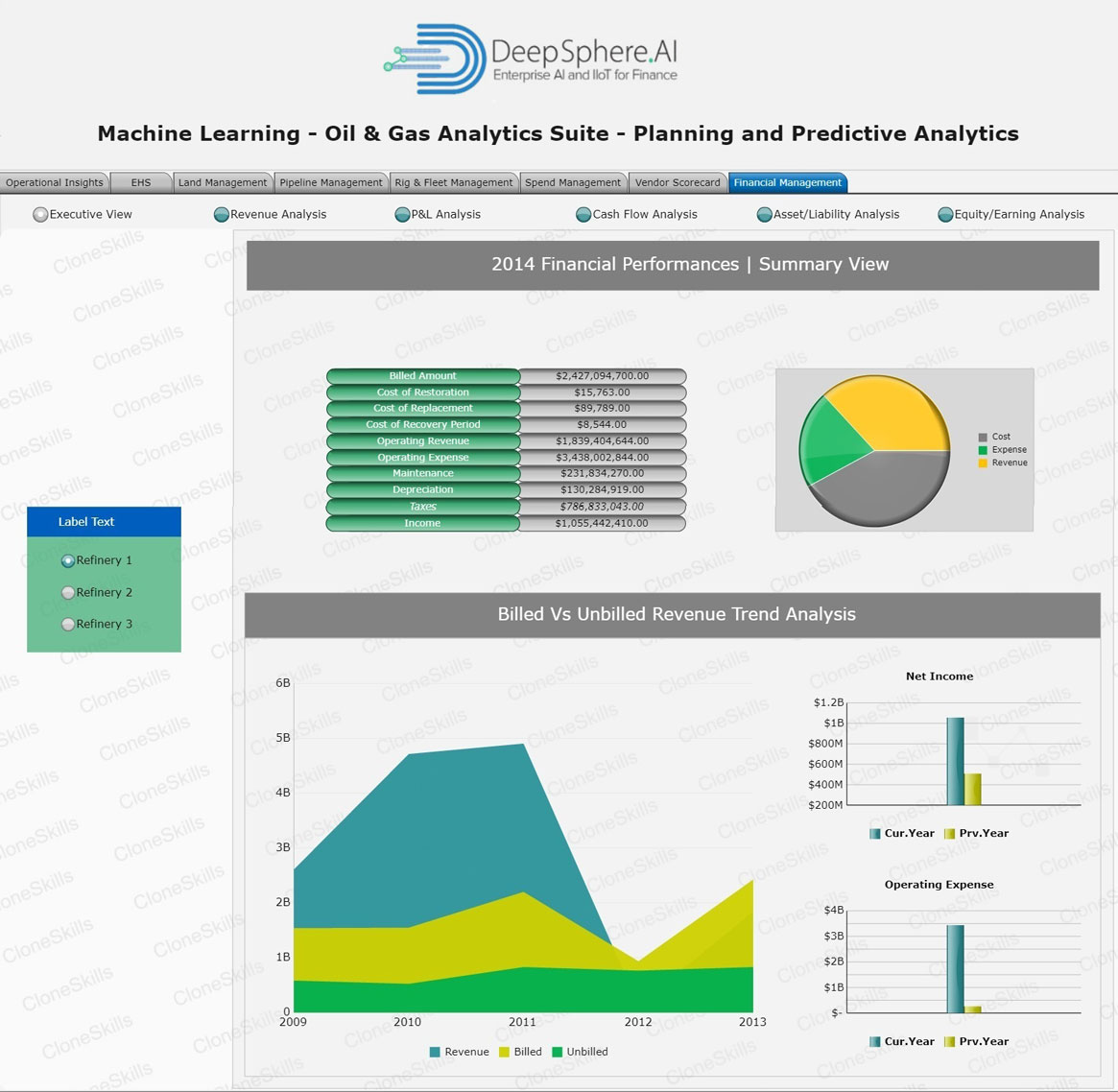

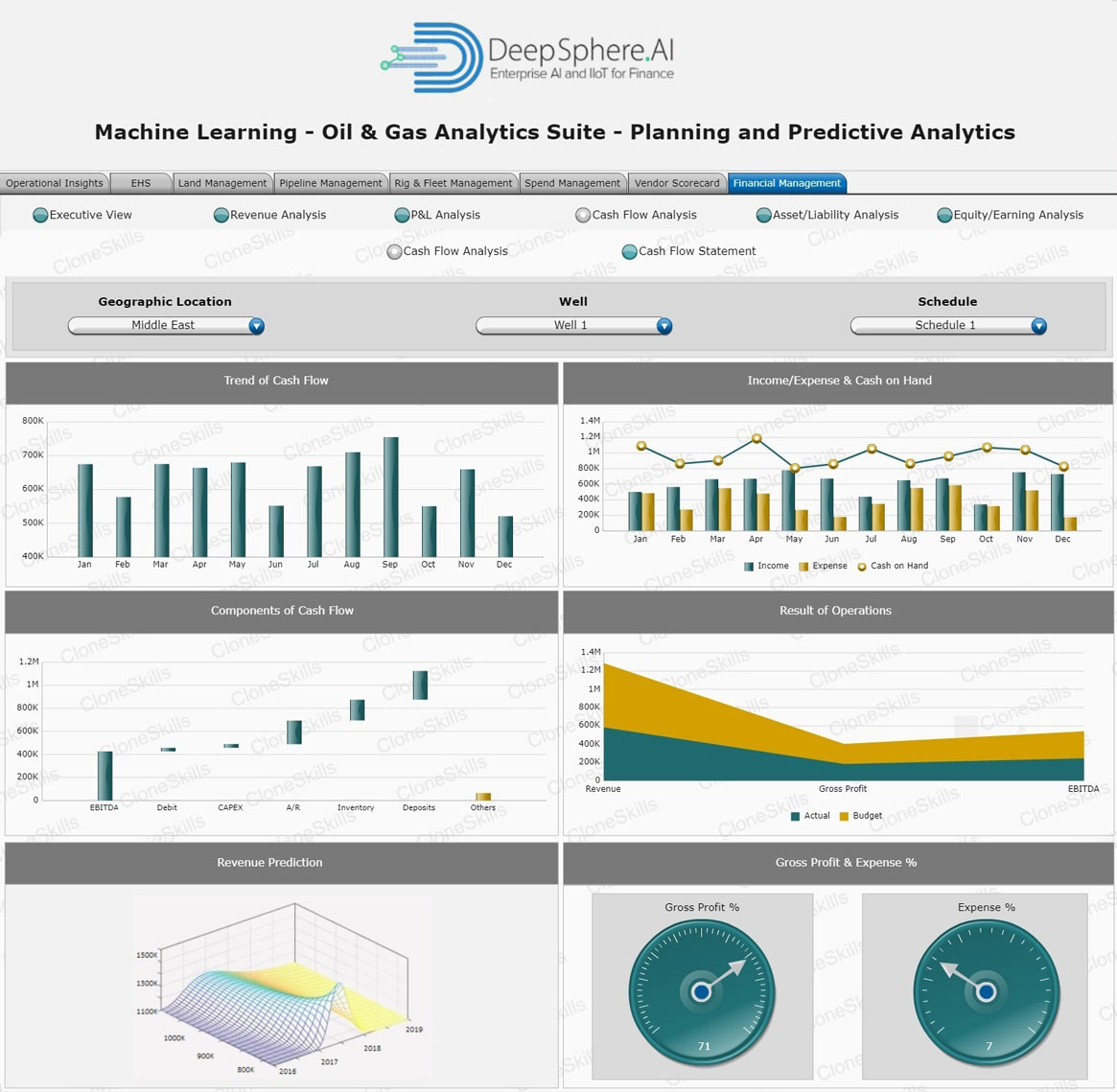

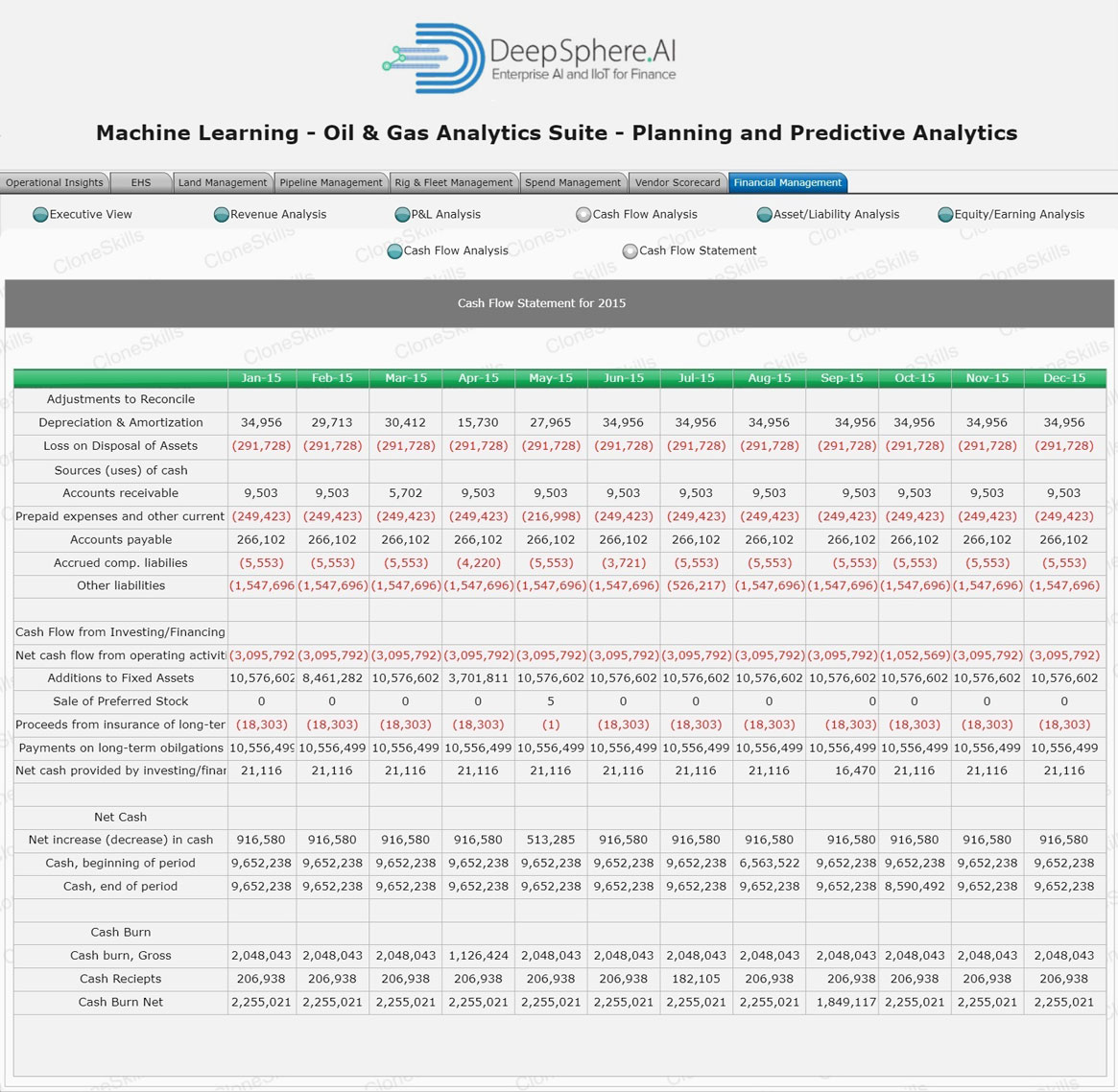

The term Oil and Gas “Net Cash Flow,”is the difference between a company's cash inflows and outflows in a given period. In the strictest sense, net cash flow refers to the change in a company's cash balance as detailed on its cash flow statement. One can approximate a company's net cash flow by looking at the period-over-period change in cash on the balance sheet. However, the statement of cash flows is a more insightful place to investigate. Net cash flow is the sum of cash flow from operations (CFO), cash flow from investing (CFI), and cash flow from financing (CFF).

Net Cash Flow is most commonly used model in the Oil and Gas industry to determine profit is the NCF model since this model incorporates the time value of money. Profit in the cash-flow model is also referred to as net cash flow (NCF). The NCF model has one unique feature and this unique piece is called time zero. Time zero is the day that the check is written to the contractors to perform a job.

CAPEX is placed in time zero in the NCF model. It is very important that the cash-flow model is used for economic analysis, since it incorporates the time value of money. Profit excluding investment is referred to as operating cash flow. Net cash flow from investment is made up of a number of components – some positive, some negative – so for example capital expenditure (CAPEX) costs of drilling wells, laying pipelines and building facilities along with operational expenditure (OPEX) must be counted against profits from selling oil or gas.

The Oil and Gas term “Net Present Value” is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Net Present Value is used in capital budgeting and investment planning to analyze the profitability of a projected investment or project.

Net Present Value, as the name indicates, calculates the net amount that the discounted cash flows of an investment exceed the initial investment. Using the discounted cash flow (DCF) formula, the future cash flows are discounted by the rate of return offered by comparable investment alternatives (i.e. the opportunity cost of capital) and then summed and added to the initial investment amount. Net Present Value is one way of analyzing the profitability of an investment. NPV is basically the value of specific stream of future cash flows presented in today’s dollar. NPV is an essential calculation in petroleum economics due to considering time value of money and inflation.

Companies are keen to know what an actual project is worth in today’s dollar rather than, say, the dollar of 10 years from now. As a simple example, Oil and Gas operating companies project the future production rates for each well using various techniques such as decline curve, type curve, reservoir simulation, rate transient analysis, material balance, and so forth. Those future production rates that will yield future cash flows must be discounted (using cost of capital) to present value. It really does not make any logical sense for a company to announce that their profit cash flows for doing a project would be $10 million, $8 million, $12 million, and $11 million in subsequently 2, 3, 4, and 5 years.

The term “Oil Price”, refers to the spot price of one barrel of the benchmark crude oil. The price depends upon its grade, location and the content of sulfur present in it. The price of oil can be determined with the help of balance between its demand and supply. Oil storage trade is a strategy in which oil is purchased by the large oil companies when the prices are low for instant storage and delivery. Large oil companies then keep the oil stored till the prices rise.

Oil Prices play an important role in the global economy. As oil is a global commodity with high demand, there is always a possibility that the large fluctuations in the prices may have a powerful impact on the global economy. The major factors which have direct impact on the Oil Prices are market sentiment, demand and supply. When the supply decreases the demand increases and the price of oil goes up and vise versa. Oil supply depends on tax, legal framework, geological discovery, political situation of the oil producing companies and the cost of extracting the oil. The oil demand depends on the macroeconomic conditions of the globe.

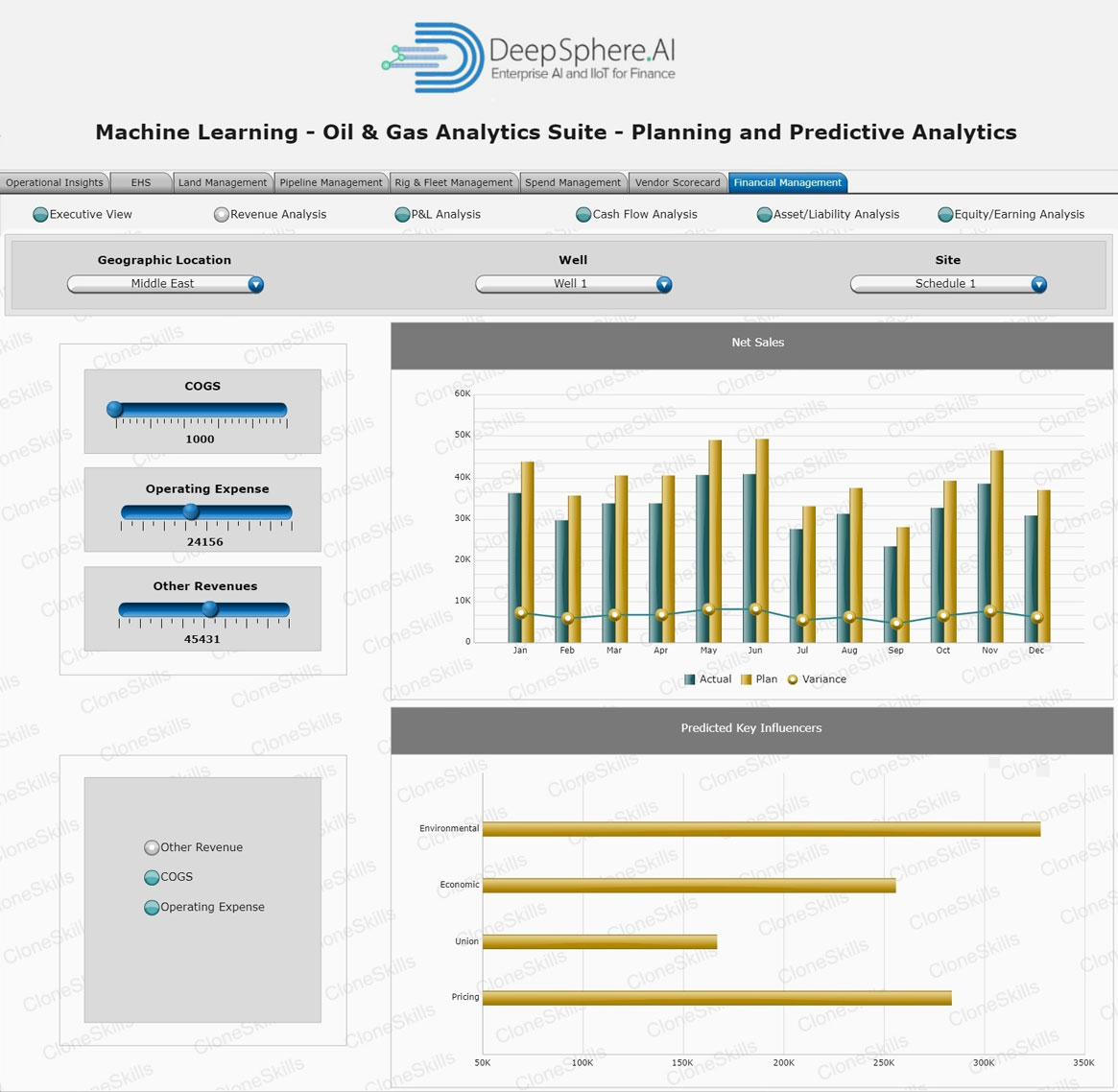

The term Oil and Gas “Operational Expenditure,”consists of those expenses that a business incurs to run smoothly every single day. They are the costs that a business incurs while in the process of turning its inventory into an end product. Hence, depreciation of fixed assets that are used in the production process is considered Operational Expenditure. OPEX is also known as an operating expenditure, revenue expenditure or an operating expense.

The Oil and Gas sector plays an important role in the economy by drilling, extracting, and processing Oil and Gas. Because operating expenses vary widely with the size of Oil and Gas companies, average operating expenses tend to be meaningless. Financial professionals typically assess the average operating expenses by looking at the average operating expenses margin, which is expressed as the percentage of operating expenses in the sector's total revenues. In July 2015, the average operating expenses margin for the oil and gas industry was approximately 33%. Given the average revenue of $60 billion over the last four quarters, the average operating expense in the Oil and Gas sector stands at approximately $19.5 billion per company.

The operating expenses margin differs widely in the Oil and Gas sector. Oil and Gas drilling companies have the highest margin among all companies, at 85% of their total revenues, resulting in a negative operating income margin of 24%. Oil and gas refining and marketing companies boast the lowest operating expenses margin of 12.4%. The largest determinant of the size of the operating expenses margin is depreciation expense and the ability of Oil and Gas companies to manage their fixed costs.

The term Oil and Gas “Royalty,” refer to funds received from the production of oil or gas, free of costs, except taxes. Oil and Gas royalties are also the cash value paid by a lessee to a lessor or to one who has acquired possession of royalty rights, based on a percentage of gross production from the property, free and clear of all costs. The word "royalty," as used in connection with Oil and Gas leases, conveyances, and reservations, has a definite meaning in its popular sense. It means a share of the products, or proceeds therefrom, reserved to the owner of land for permitting another to use the property.

Whenever oil or gas production begins, the landowner is entitled to part of the total production. A royalty is agreed upon as a percentage of the lease, minus what was reasonably used in the Lessee's production costs. The royalty is paid by the Lessee to the owner of the mineral rights, the Lessor in the Lease. It is based on a percentage of the gross production from the property and is free and clear of all costs, except for taxes.

Oil Royalties may be paid in oil. The Lessor may receive oil from the Lessee and then market the oil. Unless the Lessor is wise and understands the market, electing to receive the royalty in this manner, could be a disadvantage and the landowner, electing for this arrangement, may not benefit from it. Most landowners choose to receive the royalty in cash at the posted price of the oil. A Lessor deciding to receive the oil as the royalty payment can market the oil royalty back to the Lessee for marketing and receive cash through that arrangement.

A “Tax” is a compulsory financial charge or some other type of levy imposed upon a taxpayer (an individual or other legal entity) by a governmental organization in order to fund various public expenditures. A failure to pay, along with evasion of or resistance to taxation, is punishable by law. Taxes consist of direct or indirect taxes and may be paid in money or as its labour equivalent.

An Oil and Gas company is taxed the value of produced Oil and Gas. These taxes are applied at the point of production, before accounting for transportation and distribution costs. Value taxes can be difficult to implement because states must closely monitor gas and oil sales to determine the current market value. Furthermore, because prices are prone to fluctuation, value taxes can make state revenue predictions difficult. Texas and Wyoming tax the assessed oil and gas value with reduced rates and exemptions to incentivize production from certain well types.

Under a concession, an Oil and Gas company is granted exclusive rights to exploration and production of the concession area and owns all Oil and Gas production. Under concession an Oil and Gas company typically pays royalties and corporate income tax. Other payments to the government may be applicable, such as bonuses, rentals, resource taxes, special petroleum or windfall profit taxes, export duties, state participation and others.

Definition: The term Oil and Gas “Revenue”, typically refers to a company's revenue net of discounts and returns. Sometimes, though, the user is referring to net profit, which is sales net of all expenses. Generation of revenue is an important driver that influences the Oil and Gas industry. Operating cost of a refinery is very huge and in many instances, this will affect adversely on offshore operations.

Although the revenue generated is high, industry need to adapt itself to the global market. With the ever-increasing demand and dependence on these energy sources, it is hoped that this industry will continue to create revenue to invest in new exploration projects and technology, and the costs would gradually stabilise.

Exploration & Production companies report their Oil and Gas reserves the quantity of Oil and Gas they own that is still in the ground in the same bbl and mcf terms. Reserves are often used to value Exploration & Production companies and make predictions for their revenue and earnings. New reserves, of course, are the primary source of future revenue, so Exploration & Production companies spend a lot of time and money exploring for new petroleum reserves. If an Exploration & Production company stops exploring, it will generate revenue from a finite and depleting quantity of petroleum and revenue inevitably will decline over time.

Definition: The term Oil and Gas “Capital Expenditure, or CAPEX ”, is financing used by companies to secure physical assets or upgrade current assets. CAPEX generally takes two forms; maintenance expenditure, in which a company purchases assets that extend the useful life of existing assets, and expansion expenditure, in which a company purchases new assets in an effort to grow the business.

CAPEX is basically capital expenditures such as drilling & completing a well. It’s a critical component to capital budgeting & should be monitored well. Capital Expenditures incurred in exploration activities should be expensed unless they meet the definition of an asset. An entity recognizes an asset when it is probable that economic benefits will flow to the entity as a result of the expenditure. The economic benefits might be available through commercial exploitation of hydrocarbon reserves or sales of exploration findings or further development rights. It is difficult for an entity to demonstrate that the recovery of exploration expenditure is probable. Where entities do not adopt IFRS 6 and instead develop a policy under the Framework, expenditures on an exploration property are expensed until the capitalization point.

Definition: The term Oil and Gas “Operational Expenditure”, consists of those expenses that a business incurs to run smoothly every single day. They are the costs that a business incurs while in the process of turning its inventory into an end product. Hence, depreciation of fixed assets that are used in the production process is considered Operational expenditure. OPEX is also known as an operating expenditure, revenue expenditure or an operating expense.

The Oil and Gas sector plays an important role in the economy by drilling, extracting, and processing Oil and Gas. Because operating expenses vary widely with the size of Oil and Gas companies, average operating expenses tend to be meaningless. Financial professionals typically assess the average operating expenses by looking at the average operating expenses margin, which is expressed as the percentage of operating expenses in the sector's total revenues. In July 2015, the average operating expenses margin for the Oil and Gas industry was approximately 33%. Given the average revenue of $60 billion over the last four quarters, the average operating expense in the Oil and Gas sector stands at approximately $19.5 billion per company.

The operating expenses margin differs widely in the Oil and Gas sector. Oil and Gas drilling companies have the highest margin among all companies, at 85% of their total revenues, resulting in a negative operating income margin of 24%. Oil and Gas refining and marketing companies boast the lowest operating expenses margin of 12.4%. The largest determinant of the size of the operating expenses margin is depreciation expense and the ability of Oil and Gas companies to manage their fixed costs

Definition: The term “Oil Price”, refers to the spot price of one barrel of the benchmark crude oil. The price depends upon its grade, location and the content of sulfur present in it. The price of oil can be determined with the help of balance between its demand and supply. Oil storage trade is a strategy in which oil is purchased by the large oil companies when the prices are low for instant storage and delivery. Large oil companies then keep the oil stored till the prices rise.

Oil Prices play an important role in the global economy. As oil is a global commodity with high demand, there is always a possibility that the large fluctuations in the prices may have a powerful impact on the global economy. The major factors which have direct impact on the Oil Prices are market sentiment, demand and supply. When the supply decreases the demand increases and the price of oil goes up and vise versa. Oil supply depends on tax, legal framework, geological discovery, political situation of the oil producing companies and the cost of extracting the oil. The oil demand depends on the macroeconomic conditions of the globe.

Definition: The term “Cost of Capital” refers to the weighted average cost of various capital components, i.e. sources of finance, employed by the firm such as equity, preference or debt. In finer terms, it is the rate of return, that must be received by the firm on its investment projects, to attract investors for investing capital in the firm and to maintain its market value.

The Cost of capital (WACC), as the name implies, is the firm’s overall capital structure, i.e. its cost of equity (re) and its cost of debt (rd). The Cost of Capital is just an algebraic manipulation to combine the re and rd into their respective proportion reflecting the capital structure of the investor. Cost of Capital represents the expected return on a portfolio of all the company’s securities, i.e. equity and debt. This rate is applied to project cash flows - cash flows excluding the cash outflows due to financing (i.e. interest payment, principal payment, or the tax benefit created due to the tax deductible interest payments). The side effects of the project financing are instead bundled in the WACC

Definition: The term Oil and Gas “Net Cash Flow ”, is the difference between a company's cash inflows and outflows in a given period. In the strictest sense, net cash flow refers to the change in a company's cash balance as detailed on its cash flow statement. One can approximate a company's net cash flow by looking at the period-over-period change in cash on the balance sheet. However, the statement of cash flows is a more insightful place to look. Net cash flow is the sum of cash flow from operations (CFO), cash flow from investing (CFI), and cash flow from financing (CFF).

Net Cash Flow is most commonly used model in the Oil and Gas industry to determine profit is the NCF model since this model incorporates the time value of money. Profit in the cash-flow model is also referred to as net cash flow (NCF). The NCF model has one unique feature and this unique piece is called time zero. Time zero is the day that the check is written to the contractors to perform a job.

CAPEX is placed in time zero in the NCF model. It is very important that the cash-flow model is used for economic analysis, since it incorporates the time value of money. Profit excluding investment is referred to as operating cash flow. Net cash flow from investment is made up of a number of components – some positive, some negative – so for example capital expenditure (CAPEX) costs of drilling wells, laying pipelines and building facilities along with operational expenditure (OPEX) must be counted against profits from selling oil or gas.

Definition: The Oil and Gas term “Net Present Value ”, is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Net Present Value is used in capital budgeting and investment planning to analyze the profitability of a projected investment or project.

Net Present Value as the name indicates calculates the net amount that the discounted cash flows of an investment exceed the initial investment. Using the discounted cash flow (DCF) formula, the future cash flows are discounted by the rate of return offered by comparable investment alternatives (i.e. the opportunity cost of capital) and then summed and added to the initial investment amount. Net Present Value is one way of analyzing the profitability of an investment. NPV is basically the value of specific stream of future cash flows presented in today’s dollar. NPV is an essential calculation in petroleum economics due to considering time value of money and inflation.

Companies are keen to know what an actual project is worth in today’s dollar rather than, say, the dollar of 10 years from now. As a simple example, Oil and Gas operating companies project the future production rates for each well using various techniques such as decline curve, type curve, reservoir simulation, rate transient analysis, material balance, and so forth. Those future production rates that will yield future cash flows must be discounted (using cost of capital) to present value. It really does not make any logical sense for a company to announce that their profit cash flows for doing a project would be $10 million, $8 million, $12 million, and $11 million in subsequently 2, 3, 4, and 5 years.

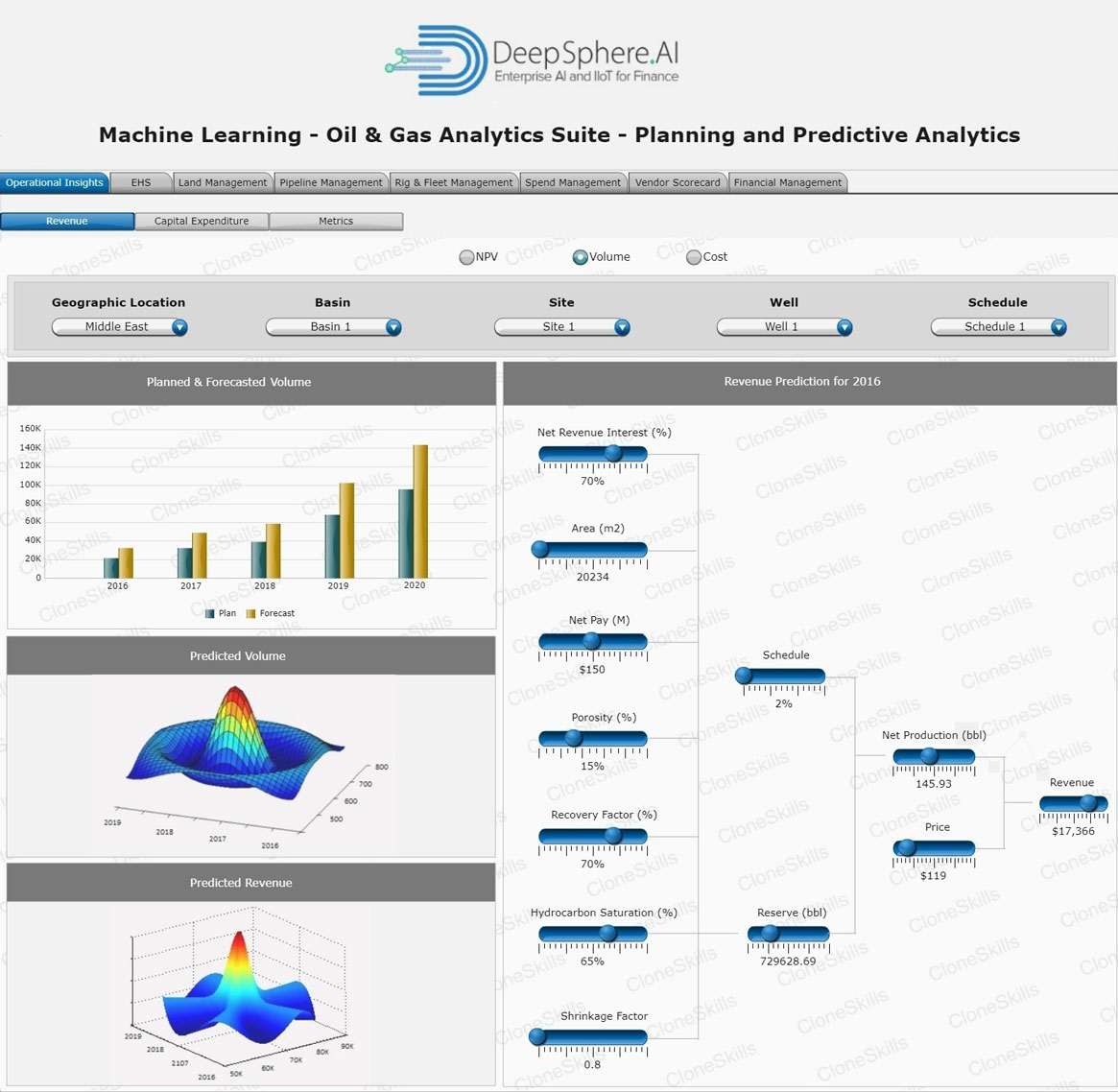

Definition: The term “Planned Volume” is defined as a plan that an Oil and Gas company lays out, typically broken down into a step-by-step format, for utilizing its available capital and other assets to meet its goals for increased production volume based on a reasonable financial forecast. A financial plan can be considered synonymous with a business plan in that it lays out what a company plans to do in terms of putting resources to work to generate maximum possible revenues.

Definition: The term “Forecasted Volume” is defined as is an estimation or projection of likely future Oil production volume. Financial forecasts are commonly reviewed and revised annually as new information regarding assets and costs becomes available. The new data enables an individual or business to make more accurate financial projections. It is easier for established companies that generate steady revenues to make accurate financial forecasts than it is for new businesses or companies whose revenue is subject to significant seasonal or cyclical fluctuations.

Definition: “Planned costs” can be defined as the costs required to plan a well properly that are insignificant in comparison to the actual drilling costs. In many cases, less than $1,000 is spent in planning a $1 million well. This represents 1/10 of 1%; of the well costs.

Unfortunately, many historical instances can be used to demonstrate that well planning costs were sacrificed or avoided in an effort to be cost conscious. The end result often is a final well cost that exceeds the amount required to drill the well, if proper planning had been exercised. Perhaps the most common attempted shortcut is to minimize data-collection work. Although good data can normally be obtained for small sums, many well plans are generated without the knowledge of possible drilling problems. This lack of expenditure in the early stages of the planning process generally results in higher-than-anticipated drilling costs.

Definition: The term “Forecasted Cost” is defined as is an estimation or projection of likely plan a well properly that are insignificant in comparison to the actual drilling costs. Financial forecasts are commonly reviewed and revised annually as new information regarding assets and costs becomes available. The new data enables an individual or business to make more accurate financial projections. It is easier for established companies that generate steady revenues to make accurate financial forecasts than it is for new businesses or companies whose revenue is subject to significant seasonal or cyclical fluctuations.

Definition: “Proven Reserves” is the quantity of natural resources that a company reasonably expects to extract from a given formation. Proven reserves are established using geological and engineering data gathered through seismic testing and exploratory drilling. In Oil and Gas extraction, once the physical shape of a formation is understood, the reservoir is estimated by fluid contacts. Fluid contacts refer to the natural layering of gas, oil and water in a formation. An accurate picture of the formation shape and known levels of fluid contact provide the data for a volume estimate with a high degree of confidence.

Proven reserves are classified as having a 90% or greater likelihood of being present and economically viable for extraction in current conditions. Proven reserves are also referred to as proved reserves. Within the oil industry, proven reserves are also referred to as P1 or P90. Proven reserves also take into account the current technology being used for extraction, regional regulations and market conditions as part of the estimation process. For this reason, proven reserves can seemingly take unexpected leaps and drops. Depending on the regional disclosure regulations, extraction companies might only disclose proven reserves even though they will have estimates for probable and possible reserves.

Understanding the natural resource extraction industry can be challenging because proven reserves are just one of three classifications. Most people assume proven Oil and Gas reserves should only go up when new exploratory wells are drilled, resulting in new reservoirs being discovered. In reality, there is often more significant gains and losses resulting from shifts between classifications than there are increases in proven reserves from truly new discoveries.

Definition: “Unproven Reserves” are based on geologic and/or engineering data similar to that used in estimates of proved reserves; but technical, contractual, economic, or regulatory uncertainties preclude such reserves being classified as proved. Unproved reserves may be further classified as probable reserves and possible reserves. Unproved reserves may be estimated assuming future economic conditions different from those prevailing at the time of the estimate. The effect of possible future improvements in economic conditions and technological developments can be expressed by allocating appropriate quantities of reserves to the probable and possible classifications.

Unproven reserves, due to regulatory or economic factors, are estimated as less recoverable and therefore unproven. This class of reserves is further broken down into subcategories of probable and possible. The SEC requires the lower certainty evaluations to be verified by a third party before an Oil and Gas company can publicly state them to potential investors.

Unproven Reserve is a geologically equivalent to proven reserves, their unproven status rests on technical, regulatory, or political issues. Unproven reserves fall into two categories: probable and possible. A probable reserve has a 50% chance for petroleum recovery and is termed in the industry P50. A possible reserve, also called a P10 reserve, has a 10% chance of recovery.

Definition: The term “Exploration Costs” is defined as the costs an oil or gas company incurs while searching for oil or gas to drill. Exploration costs include the cost of researching appropriate places to drill and the cost of actually drilling. There is no guarantee that there will be a return on the investment of exploration costs because there is no guarantee that the company will find oil or natural gas. Exploration costs can also be quite expensive.

Exploration Costs (including prospecting) related to Oil and Gas producing entities and would be included in operating expenses of that entity. Costs incurred in identifying areas that may warrant examination and in examining specific areas that are considered to have prospects of containing Oil and Gas reserves, including costs of drilling exploratory wells and exploratory-type stratigraphic test wells. Exploration costs may be incurred both before acquiring the related property (sometimes referred to in part as prospecting costs) and after acquiring the property. Principal types of exploration costs, which include depreciation and applicable operating costs of support equipment and facilities and other costs of exploration activities.

Exploration costs are incurred to discover hydrocarbon resources. Evaluation costs are incurred to assess the technical feasibility and commercial viability of the resources found. Exploration, as defined in IFRS 6 Exploration and evaluation of mineral resources, starts when the legal rights to explore have been obtained. Expenditure incurred before obtaining the legal right to explore is generally expensed; an exception to this would be separately acquired intangible assets such as payment for an option to obtain legal rights.

Definition: “Development Costs” are costs incurred to obtain access to proved reserves and to provide facilities for extracting, treating, gathering and storing the Oil and Gas. An entity should develop an accounting policy for development expenditure based on the guidance in IAS 16, IAS 38 and the Framework. Much development Costs results in assets that meet the recognition criteria in IFRS. 22 Development Costs are capitalised to the extent that they are necessary to bring the property to commercial production.

Entities should also consider the extent to which abnormal costs have been incurred in developing the asset. IAS 16 requires that the cost of abnormal amounts of labor or other resources involved in constructing an asset should not be included in the cost of that asset. Entities will sometimes encounter difficulties in their drilling plans and make adjustments to these, with the side track issue discussed in section 2.3.8 being one example. There will be a cost associated with this, and entities should develop a policy on how such costs are assessed as being normal or abnormal.

Costs incurred after the point at which commercial production has commenced should only be capitalized if the expenditures meet the asset recognition criteria in IAS 16 or 38.

Definition: “Production Costs” (also called Lifting Costs) are the costs to operate and maintain wells and related equipment and facilities per barrel of oil equivalent (BOE) of Oil and Gas produced by those facilities after the hydrocarbons have been found, acquired, and developed for production. Direct lifting costs are total production spending minus production taxes (and also minus royalties in foreign regions) divided by oil and natural gas production in BOE. Total lifting costs are the sum of direct lifting costs and production taxes.

Productions Costs are also defined as the costs associated with the operation of Oil and Gas wells to bring hydrocarbons to the surface after wells (facilities necessary for the production of oil) have been drilled. This figure includes labor costs, electricity costs and maintenance costs. Non-income related taxes: as production of hydrocarbons is such a lucrative business, governments also want to have their shares. There exists an abundance of different model how the state can profit from hydrocarbon production (profit sharing, royalties, etc.).

Production Operations is responsible to manage and optimize Production costs. Productions costs are also often called Lease Operating Expense (LOE). It is the job of analysts to allocate production costs between Oil and Gas using relative production weightings, with oil today generally receiving a greater share of the cost.

Definition: The term “Enhanced Recovery” is defined as the amount an Oil and Gas company invests on Enhanced oil recovery processes. Enhanced oil recovery (EOR) is the technique or process where the physicochemical (physical and chemical) properties of the rock are changed to enhance the recovery of hydrocarbon. The properties of the reservoir fluid system which are affected by EOR process are chemical, biochemical, density, miscibility, interfacial tension (IFT)/surface tension (ST), viscosity and thermal. EOR often is called tertiary recovery if it is performed after waterflooding.

Sophisticated equipment and complex technologies are required to recover natural gas from underground reservoirs. But depending on the geology of these areas, this fuel can never be completely removed. The natural pressure in gas pockets usually limits yield to around 75 percent and a maximum of 50 percent in the case of oil. But there are methods with which natural gas can still be extracted, even after recovery is quite far along. One useful tool is nitrogen (N2).According to studies by independent research institutes, nitrogen (N2) or carbon dioxide (CO2) can be used to increase the pressure in Oil and Gas fields and thus improve the output. This reduces delays or drops in the recovery rate.

Definition: The term “Improved Recovery” is defined as the amount an Oil and Gas company invests on Improved recovery processes. Improved Recovery is a method used to recover the additional oil left after rock compressibility, fluid expansion, pressure decline, natural gas drive or water drive and gravitational drainage. The process involves the implementation of several artificial techniques to increase the amount of fluids which can be extracted from oilfields.

There are three dominant techniques that are used for Improved Recovery, i.e., gas injection, chemical injection and thermal injection. It also includes gas cycling, pressure maintenance, enhanced recovery and secondary recovery. Improved Recovery is also known as improved oil recovery, enhanced oil recovery and tertiary recovery. It is a process like gas flooding or waterflooding which adds energy to reservoirs for increasing the recovery factor and stimulating the oil production.

Definition: The term “Proved Reserve Acquisition Costs” are the costs incurred by an Oil and Gas company on Acquiring Proved Reserves. Proved Reserves is the quantity of natural resources that a company reasonably expects to extract from a given formation. Proven reserves are established using geological and engineering data gathered through seismic testing and exploratory drilling. In Oil and Gas extraction, once the physical shape of a formation is understood, the reservoir is estimated by fluid contacts. Fluid contacts refer to the natural layering of gas, oil and water in a formation. An accurate picture of the formation shape and known levels of fluid contact provide the data for a volume estimate with a high degree of confidence.

Proven reserves are classified as having a 90% or greater likelihood of being present and economically viable for extraction in current conditions. Proven reserves are also referred to as proved reserves. Within the oil industry, proven reserves are also referred to as P1 or P90. Proven reserves also take into account the current technology being used for extraction, regional regulations and market conditions as part of the estimation process. For this reason, proven reserves can seemingly take unexpected leaps and drops. Depending on the regional disclosure regulations, extraction companies might only disclose proven reserves even though they will have estimates for probable and possible reserves.

Definition: The term “Finding and Development (F&D)” refers to costs incurred when a company purchases, researches and develops properties in an effort to establish commodity reserves. Exploration and development businesses rely on finding commodities to manufacture and sell. Finding and development costs represent a cost of doing business for these types of companies. The costs are calculated by dividing the costs incurred during a period of time by the number of commodities found during that same time. Oil is usually measured in barrels; gas is often measured by a given quantity of cubic feet.

While the term finding and development can relate to costs incurred by any type of commodity company, it is commonly used in regards to the upstream costs of an oil or gas business. In this case, the costs of finding and development can be expressed per barrel. Finding costs are calculated over a given period of time. During that period, the amount of money spent to locate additional commodity reserves is tallied then divided by the additional quantity of reserves actually discovered during that same time period.

Finding and Development Cost is an important performance measure that is used to evaluate Oil and Gas operations of oil companies, and it considered a tool to measure the company’s performance. This also gives a yardstick to measure a company’s ability to establish a long-term trend of adding reserves and resources at a reasonable cost.

Definition: The term “Reserve Replacement Costs” refers to cost incurred by an upstream company by considering a per-barrel-of-oil equivalent of the new reserve. Reserve Replacement Cost has a direct bearing on the future profitability of any upstream company. If a company’s Reserve Replacement Cost is too high compared to peers, it’s generally not good for the future margins or future profitability of the company.

Reserve replacement cost (RRC) is calculated by dividing development, exploitation, exploration and acquisition capital expenditures, reduced by proceeds of divestitures, for the period by net estimated proved reserve additions for the period from all sources, including acquisitions and divestitures. Our calculation of reserve replacement cost includes costs and reserve additions related to the purchase of proved reserves. The methods we use to calculate our reserve replacement cost may differ significantly from methods used by other companies to compute similar measures. As a result, our reserve replacement cost may not be comparable to similar measures provided by other companies. We believe that providing a measure of reserve replacement cost is useful in evaluating the cost, on a per-Mcfe basis, to add proved reserves.

However, this measure is provided in addition to, and not as an alternative for, and should be read in conjunction with, the information contained in our financial statements prepared in accordance with generally accepted accounting principles. Due to various factors, including timing differences in the addition of proved reserves and the related costs to develop those reserves, reserve replacement costs do not necessarily reflect precisely the costs associated with particular reserves.

Definition: The term “Recovery Factor” is a function of the displacement mechanism. An important objective of enhanced oil recovery is to increase the recovery factor. The recoverable amount of hydrocarbon initially in place, normally expressed as a percentage.

The lifecycle of an oilfield is typically characterized by three main stages: production buildup, plateau production, and declining production. Sustaining the required production levels over the duration of the lifecycle requires a good understanding of and the ability to control the recovery mechanisms involved. Increasing the recovery factor of maturing waterflooding projects by 10 to 30% could contribute significantly to the much-needed energy supply. To accomplish this, operators and service companies need to find ways to maximize recovery while minimizing operational costs and environmental imprint.

For primary recovery (i.e., natural depletion of reservoir pressure), the lifecycle is generally short and the recovery factor does not exceed 20% in most cases. For secondary recovery, relying on either natural or artificial water or gas injection, the incremental recovery ranges from 15 to 25%. Globally, the overall recovery factors for combined primary and secondary recovery range between 35 and 45%. Increasing the recovery factor of maturing waterflooding projects by 10 to 30% could contribute significantly to the much-needed energy supply. To accomplish this, operators and service companies need to find ways to maximize recovery while minimizing operational costs and environmental imprint.

Definition: The term “Estimated Ultimate Recovery (EUR)” is defined as an approximation of the quantity of oil or gas that is potentially recoverable or has already been recovered from a reserve or well. Estimated ultimate recovery can be calculated using many differing methods and units depending on the project or study being conducted. In the Oil and Gas industry, it is of the utmost importance that drilling projects meet an acceptable EUR threshold for a project to be considered viable and profitable.

Part of an oil field's probable and possible reserves are converted into proven reserves over time. These reserves can be recategorized for a number of reasons ranging from improvements in oil recovery methods and techniques to changing oil prices. For example, as oil prices rise, the quantity of proven reserves also rises because the breakeven price of recovery can be met. Reserves that were too expensive to produce at lower oil prices become viable as oil prices rise. This makes it possible to reclassify these more costly reserves as proven. The opposite happens as oil prices fall. If oil reserves become too expensive to recover at current market prices, the probability of them being produced also falls. This results in reserves being reclassified from proven back to probable or even possible.

Without an estimated ultimate recovery, oil companies would not be able to make rational investment decisions. Like all projects, management needs to be able to estimate accurately the net present value (NPV) of an oil drilling project. This valuation exercise requires several inputs, like the cost of bringing the first barrel to production, the cost of capital, the long-term price of oil and the ultimate amount of oil that will be produced, or EUR. Without an EUR, it would not be possible to reach an accurate valuation of the potential oil reserves.

Definition: The term “Lost Time Injury Frequency” is defined as the number of lost time injuries occurring in a workplace per 1 million hours worked. An Lost Time Injury Frequency of 7, for example, shows that 7 lost time injuries occur on a jobsite every 1 million hours worked. The formula gives a picture of how safe a workplace is for its workers. Lost time injuries (LTI) include all on-the-job injuries that require a person to stay away from work more than 24 hours, or which result in death or permanent disability.

Lost Time Injury Frequency is a crude indicator of safety performance and it should be considered alongside other metrics. As businesses work to reduce incidents and injuries among their employees, it’s natural to look for some way to quantify that progress. While it may be subject to some controversy, the lost time injury frequency rate (LTIFR) is one way to do it. An organization’s lost time injury frequency rate is a proxy measurement of its safety performance. It represents the number of lost time injuries that have occurred within a given accounting period, relative to the total number of hours worked in that period. It’s a lagging indicator of safety performance that can help businesses benchmark the HSE performance of their industry.

Since the Lost Time Injury Frequency number is always quite small, it’s standard practice to multiply it by 200,000 (though note that some companies and industries use a base rate of 1,000,000 instead). Companies, then, report the figure as the number of lost time injuries per million hours worked.

Definition: The term “Recordable Injury Rate” is defined as the number of fatalities, lost time injuries, substitute work, and other injuries requiring treatment by a medical professional per million hours worked. A company's recordable injury frequency rate is one of many metrics that companies can use to assess their safety performance and may be required to compile it by OSH regulations. Recordable Injury Rate is a lagging indicator of safety, meaning it represents the company's past safety performance but does not give us solid grounds to predict its future incident rate.

The Recordable Injury Rate is not to be confused with the similarly named lost time injury frequency rate. This latter metric is limited to the number of fatalities and lost time injuries per million employees and does not include other types of injuries. Recordable Incident Rate (or Incident Rate) is calculated by multiplying the number of recordable cases by 200,000, and then dividing that number by the number of labor hours at the company.

Smaller companies that experience recordable incidents will most likely have high incident rates, or the incident rates will fluctuate significantly from year to year. This is because of the small number of employees (and hence the lower number of labor hours worked) at the company. Calculations are more meaningful at larger companies that have a higher labor hour count.

Definition: The term “Fatalities” is defined as the number of death of human caused by an accident, or is the quality of the disaster being able to cause the death of a human(s). Fatality in the context of occupational health and safety is a death caused by an accident at the workplace, on the way to and from the workplace, or during other works or movements directly or indirectly related to the occupation.

Drilling is an inherently dangerous undertaking, with a fatality rate nearly five times that of all industries. The number of workers exposed to death, injury and illness in the upstream portion of the Oil and Gas industry exploration and production is growing.

Definition: The term “Fatal Accident Rates” is defined as a measure of individual risk expressed as the estimated number of fatalities per 108 exposure hours (roughly 1000 employee working lifetimes). Fatal Accidents are an increasingly rare occurrence when it comes to oil rigs. On an oil rig there are many components at work, and you’re essentially channelling flammable materials all around you.

Each time a disaster happens, engineers learn something new about how to prevent disasters and make the oil rig as a whole a safer environment to work in. The Oil and Gas Well Drilling Industries can quickly become one of the most dangerous enterprises of all if safety is bypassed. Out of the documented injuries that have occurred in this sector, there was reportedly a twenty-seven percent fatality rate increase seen from 2013 to 2014, with 142 fatal injuries, making the rate nearly 16 deaths per 100,000 workers. These increases almost make it the highest fatality rate of all job sectors.

Definition: The term “Occupational Illness” is defined as a illness that is a chronic ailment caused by exposure typically over a prolonged period to workplace hazards or work activities. It’s hard to prevent occupational illnesses because work is often difficult to spot and regulate. An illness usually develops over time, and as a result, the connection between cause and effect is not immediately obvious. By the time you notice it, the illness may require extensive treatment or could be permanent.

Health and safety has been prioritized in oil and gas industry for many years. Still, occupational hygiene exposures are often taken with proper care to determine the true risk to workers. Oil and gas workers exposed to chemicals produced and used in Oil and Gas industry may suffer occupational diseases of lungs, skin and other organs at levels relying on the amount and length of exposure time. Those exposed to hazardous noise levels may suffer noise-induced hearing loss (NIHL). Other hazards include confined spaces that may injury or threaten life of untrainedworkers.

Definition: The term “Economic Cost due to Illness” is defined as Estimating total costs incurred because of a disease or condition. Cost-of-illness analysis typically includes the value of medical care resources used to treat a disease and the losses in productivity to society because of the illness. Non-medical costs associated with the illness are sometimes included as well.

Decreased or lost productivity can be the result of illness, premature death, side effects of illness or treatment, or time spending receiving treatment. This not only affects the employee but also the family members, who reduce or stop their employment to take care of the employee. With premature death, the indirect cost is the loss in potential wage and benefits.

Cost analysis gives an indication of the financial impact of disease, and provides information to policy makers, researchers, and medical specialists that can be considered in making more efficient use of resources. Additionally, on the basis of distinction between different cost components, it may be possible to estimate the financial aspect of various treatment strategies, which can influence the choice of treatment.

Definition: The term “Oil Spill Costs” is defined as costs incurred to prevent oil spills. An oil spill of heavy fuel oil, which could devastate fragile world and destroy food sources for arctic communities, is the top threat associated with increased Arctic shipping. Heavy fuel oil is extremely toxic and slow to degrade. Oil spill response in the remote Arctic is virtually non-existent.

Definition: The term “Gas Emission” is defined as the emission into the earth's atmosphere of any of various gases, especially carbon dioxide, that contribute to the greenhouse effect. Greenhouse gases include carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O), occurring naturally and as the result of human activity.

Indirect greenhouse gas (GHG) emissions from Oil and Gas operations, including both carbon dioxide and methane emissions, today are around 5 200 million tones (Mt) of carbon-dioxide equivalent. These emissions which do not include any emissions associated with the actual consumption of the fuel amount to around 15% of the energy sector’s total GHG emissions. For gas, indirect emissions sources are between 15% and 40% of its full lifecycle emissions intensity. This means that around 97% of gas consumed today has a lower lifecycle emissions intensity than coal. Nevertheless, the aim for the future should be to focus on cost-effective ways to minimize the gap between gas and zero-carbon technologies rather than focus on the gap between coal and gas.

Definition: Oil company “Assets” are classified in three main divisions: upstream, midstream and downstream. Upstream operations are the exploration for Oil and Gas and the appraisal, development and production of any discovery, and most oil companies do not own equipment for upstream activities; they hire contractors to perform services such as geophysical surveys, well drilling and geological and environmental studies. Midstream assets are linked to the initial processing, storage and transportation of oil and gas. Crude oil refining into products such as gasoline, kerosene and diesel is a downstream activity, as is the product distribution to and marketing by a retail network.

Definition: The term “Asset Value” represents the net value of an entity and is calculated as the total value of the entity’s assets minus the total value of its liabilities. In the context of companies and business entities, the difference between the assets and the liabilities is known as the net assets or the net worth or the capital of the company.

In restructurings involving Oil and Gas reserves, the asset valuation analyses are often more complex because of the technical data and skillset required to value these reserves. Although valuing Oil and Gas assets is not necessarily more difficult than valuing other asset classes, valuing these types of assets requires a detailed understanding of the relative merits of traditional valuation methods.

Valuing Oil and Gas assets, which comprise a depleting asset base where value is correlated to constantly changing commodity prices and historical production trends, demands a thorough understanding of the technical details included in a company’s reserve database. Although commodity prices fluctuate, the value estimates of the underlying Oil and Gas assets should be based on current conditions, and are not intended to reflect unforeseeable economic or environmental events that could alter the fair market value subsequent to the valuation date.

Definition: The term “Proven reserves” is the quantity of natural resources that a company reasonably expects to extract from a given formation. Proven reserves are established using geological and engineering data gathered through seismic testing and exploratory drilling. In Oil and Gas extraction, once the physical shape of a formation is understood, the reservoir is estimated by fluid contacts. Fluid contacts refer to the natural layering of gas, oil and water in a formation. An accurate picture of the formation shape and known levels of fluid contact provide the data for a volume estimate with a high degree of confidence. Proven reserves are classified as having a 90% or greater likelihood of being present and economically viable for extraction in current conditions. Proven reserves are also referred to as proved reserves.

Proven reserves also take into account the current technology being used for extraction, regional regulations and market conditions as part of the estimation process. For this reason, proven reserves can seemingly take unexpected leaps and drops. Depending on the regional disclosure regulations, extraction companies might only disclose proven reserves even though they will have estimates for probable and possible reserves.

Definition: The term “Oil Lease” is essentially an agreement between parties to allow a Lessee (the Oil and Gas company and their production crew) to have access to the property and minerals (Oil and Gas) on the property of the Lessor. The lease agreement is a legal contract of terms. It contains certain elements, which confirm all the terms of the agreement. The lease must be dated and the lease also sets the time that the lease is effective. It establishes the primary term of the lease.

Of great importance to the landowner, the Lessor, is the royalty clause. This clause states the percentage or share of production proceeds that the Lessor receives and how the royalty is received. The Lessee is given rights in the drilling and delay rental clause. This allows the Lessee to defer immediate use of the property if the Lessee completes the obligation within a period of time and pays delay rental.

Definition: There are numerous terms and conditions listed in an Oil and Gas lease. One is “Pooling”, and it is contained in most leases. In most states, landowners may be subjected to two types of pooling arrangements. One is voluntary and the other is compulsory or statutory. In order for pooling to occur, the mineral rights’ owner must consent. By consenting to a pooling arrangement, the landowner must be careful because the utilization of pooling can materially alter the lease provisions. For example, potential royalties can be significantly reduced because the pooling provisions reduce the number of wells necessary to keep the lease in effect.

Pooling is the combination of all or portions of multiple oil and gas leases to form a unit for the drilling of a single oil and/or gas well. The unit is generally one or a combination of government survey quarter-quarter sections. Generally the interest owners in the pooled unit share the revenue from the well on the basis of surface acreage or mineral acreage owned by each interest owner in the pooled unit.

Pooling can impact the lease provisions, which may provide some unpleasant surprises as to the extent it can impact the lease. (We will discuss these in part 2 of this series.) Here are some things landowners might want to keep in mind when granting the rights to pool the leased premises. These can prevent unexpected and negative consequences from granting the right to pool.

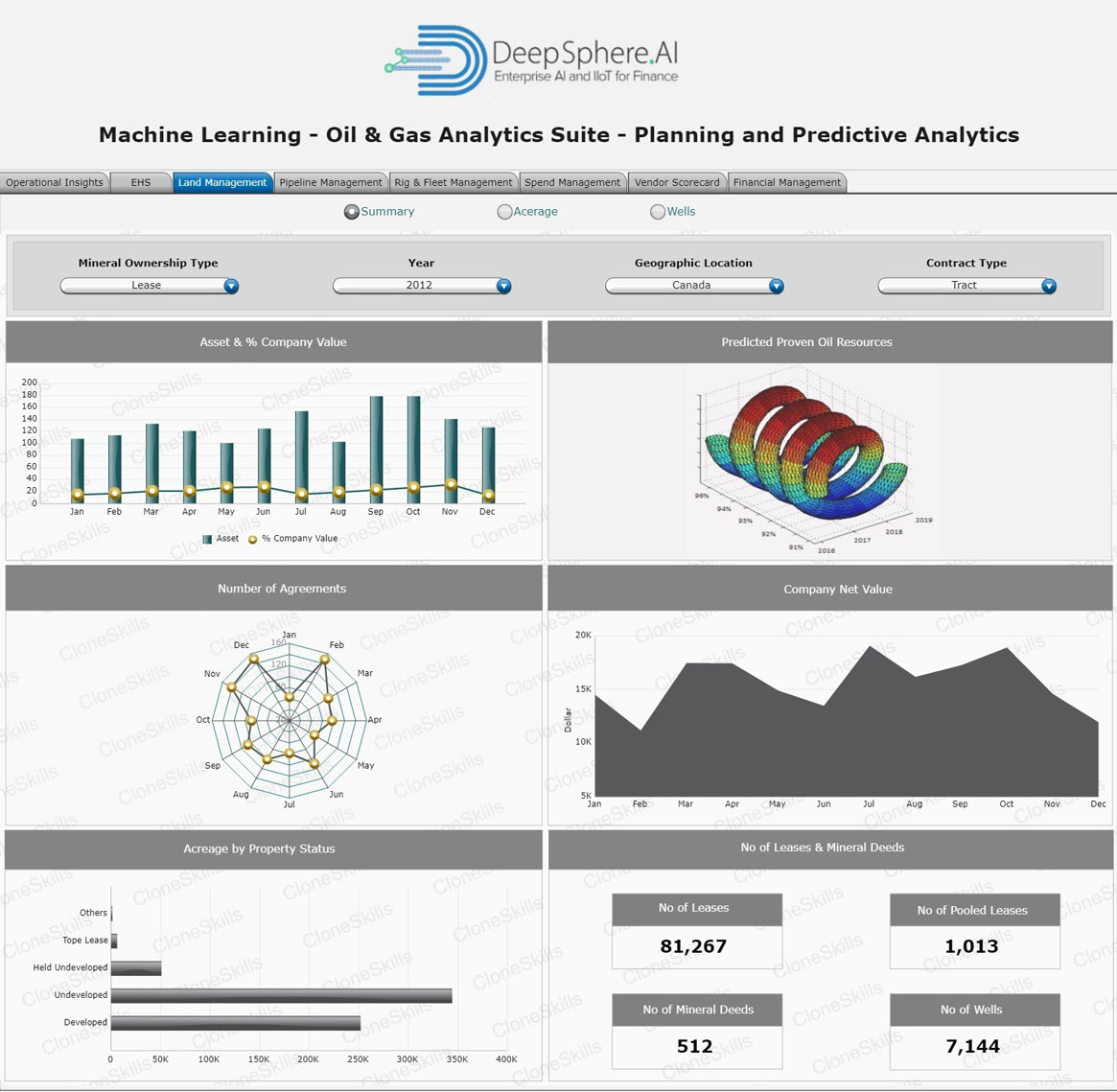

Definition: A “Mineral Deed” is a legal document which contains the details about the transfer of any mineral rights, royalty interests and overriding royalty interest owned by any royalty interest owner to Oil and Gas mineral acquisition organizations or any drilling organization with a warranty of title or without a warranty of title. If the title is not warranted in a legal document, then this mineral deed is considered as a quitclaim deed.

In the Oil and Gas industry, the entity who owns the mineral rights is called the grantor and when the grantor transfers royalty interests to another entity, the other entity is called the grantee. In simple terms an owner of the property or a grantor can own surface area of the property as well as minerals down below the property. Both the surface area of a property and the minerals below this surface area are treated as two separate legal interests. If these rights need to be transferred to any other entity, such as Oil and Gas operating organizations or minerals and royalty acquisition organizations, it can be done by signing the mineral deed which legally conveys the actual rights to the minerals while still remaining separate from the surface rights.

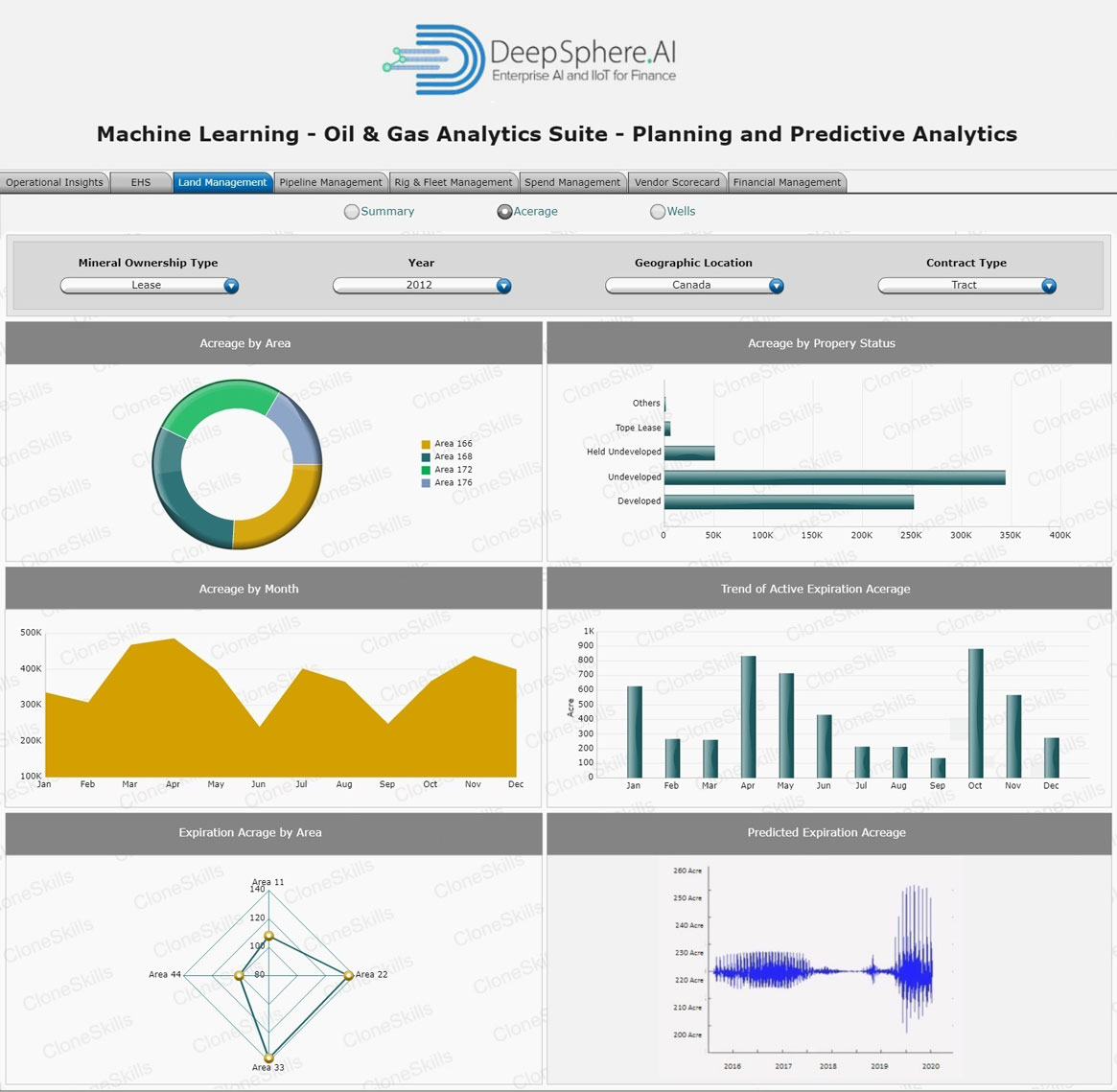

Definition: The term “Acreage” is defined as the amount of leased real estate that a petroleum and/or natural gas company has a working interest in. Gross Acreage is different from net acreage if a company shares its working interest with another company or companies. The company's true interest is expressed in net acres. Net acreage is calculated by multiplying the company's percentage interest by the gross acreage. If a company holds the entire working interest, its net acreage and gross acreage will be the same.

A company's number of gross acreage is an indication to investors of the company's size, market position and current activity. However, a company's acreage does not tell the whole story. A potential investor needs to investigate what the company is doing with that acreage. Is it drilling wells? If so, at what pace? How many barrels of oil is the area producing and how many is it expected to produce?

Larger companies will usually have an interest in hundreds of thousands of gross acres, while smaller ones may only have an interest in tens of thousands of gross acres. The largest companies will have total holdings of millions of gross acres.

Definition: The primary lease term has an ending date that applies if the land is not actually drilled or producing minerals for the lessee. If at this date nothing is being done on the land, the lease expires. This changes completely if the lessee is in the process of drilling whether producing gas and oil or not. If there is active exploration or drilling going on that began prior to the primary term's expiration date, the lease is still considered to be in effect provided the company does not stop work for longer than 90 days.

In other words, as long as a lessee engages in drilling even one day prior to the end of the contract, they are allowed to keep doing so to either produce minerals or determine a well is dry. The lessee can drill as many holes as they wish, exploring beyond the lease expiration date, provided they continue to do so with the intent to produce. This automatic extension is said to be the secondary lease term.

When leasing gas and oil rights, when the secondary lease term goes into effect there certain things can happen. The drilling company can continue exploring the land until they begin to produce Oil and Gas, regardless of how long that takes as long as efforts do not lapse for greater than 90 days. If and when they are able to produce minerals, they are also permitted to continue doing so provided they do not cease production for longer than 60 days.

Definition: An “Oil Well” is a boring in the Earth that is designed to bring petroleum oil hydrocarbons to the surface. Usually some natural gas is released along with the oil. A well that is designed to produce only gas may be termed a gas well. There are numerous different ways that oil well can be drilled to maximize the output of the well while minimizing other costs. The most common type of well drilled today is known as a conventional well. These wells are wells drilled in the traditional sense in that a location is chosen above the reservoir and the well is drilled vertically downward. Additionally, wells with a small amount of deviation in their path from the vertical are also considered to be conventional. This slight turning of the well is obtained during drilling by using a type of steerable device that shifts the direction the well is being dug. These wells are the most common and are fairly inexpensive to drill.

Horizontal wells are an alternative type of well used when conventional wells do not yield enough fuel. These wells are drilled and steered to enter a deposit nearly horizontally. These wells can hit targets and stimulate reservoirs in ways that a vertical well cannot. Combined with hydraulic fracturing previously unproductive rocks can be used as sources for natural gas. Examples of these types of deposits include formations that contain shale gas or tight gas.

Other types of wells include offshore wells, which are wells that are drilled in the water instead of onshore. These provide access to previous inaccessible oil deposits. Multilateral wells are wells used occasionally that have several branches off of the main borehole that drain a separate part of the reservoir.

Definition: The term “High Consequence Area Miles” is a buffer that usually extends 660 feet (200 meters) to either side of a segment of pipeline which passes through developed areas where people live in an urban or suburban setting, or where they frequently gather, like a school. Pipelines within an HCA are required to have extra safety features or extra precautions must be taken by pipeline operators depending on the type of pipeline, the material being conveyed, and other factors.

Although commonly assumed to run through areas with a high population density, that is not the full picture of how HCAs are designated. There is a detailed process that pipeline operators (the pipeline companies) must follow to determine where an HCA is located. Pipeline operators are required to establish and implement a higher level of safety features for pipelines within an HCA compared to pipelines outside an HCA. Thus, any property within an HCA will have greater safety protections.

A random pipeline leak or some other malfunction could possibly occur on any segment of a given pipeline, either inside or outside an HCA. However, because the land within an HCA is usually more densely populated, a leak inside an HCA could cause more harm and injuries than the very same sort of leak outside an HCA. In other words, there are more safety provisions with an HCA because more people are living or gathering there. It is not the type or condition of the pipeline which causes a HCA to be established, but rather the population density, types of land use, and features of the lands near the pipeline.

Definition: An operator is required to temporarily reduce operating pressure or shut down the pipeline until the operator could complete the repair, basing the temporary operating pressure reduction on remaining wall thickness. immediate repair conditions are those where the indicated anomaly may suggest the potential for imminent failure. However, API objected to limiting an operator's actions to address these conditions to repair of the condition. API recommended renaming these immediate concern conditions, and allowing an operator to take actions other than repair.

To maintain safety, an operator must temporarily reduce the operating pressure or shut down the pipeline until the operator completes the repair of these conditions. An operator must calculate the temporary reduction in operating pressure. If no suitable remaining strength calculation method can be identified, an operator must implement a minimum 20 percent or greater operating pressure reduction, based on actual operating pressure for two months prior to the date of inspection, until the anomaly is repaired.

Definition: Many pipeline accidents have proven that the damage from a leak that impacts a high consequence area, known as a HCA, is greatly compounded and endures far longer than leaks elsewhere. HCAs also include populated areas and sensitive ecological resources including locations where federally listed threatened and endangered species can be found, and areas where migratory water birds concentrate. Good engineering practices and pipeline regulations require pipeline operators to augment the leak detection systems on sections where a pipeline failure could affect a high consequence area.

The leak detection systems that cover the entire length of a cross-country pipeline often lack sufficient intermediate sensors and are limited in their ability to detect and locate very small leaks close to a HCA. If a secondary leak detection system is added with sensors installed immediately upstream, and downstream of the HCA section, this new system can be tuned to much higher sensitivity, as its sensors will isolate the HCA section from influences elsewhere along the pipeline.

Definition: The failure of a high-pressure natural gas pipeline can lead to various outcomes, some of which can pose a significant threat to people and property in the immediate vicinity of the failure location. The dominant hazard is thermal radiation from a sustained jet or trench fire. An estimate of the ground area affected by a credible worst-case failure event can be obtained from a model that characterizes the heat intensity associated with rupture failure of the pipe where the escaping gas is assumed to feed a sustained trench fire that ignites very soon after line failure.

An equation has been developed that relates the diameter and operating pressure of a pipeline to the size of the area likely to experience high consequences in the event of an ignited rupture failure. The model upon which the hazard area equation is based consists of three parts: 1) a fire model that relates the rate of gas release to the heat intensity of the fire as a function of distance from the fire source; 2) an effective release rate model that provides a representative steady-state approximation to the actual transient release rate; and 3) a heat intensity threshold that establishes the sustained heat intensity level above which the effects on people and property are consistent with the adopted definition of a so-called High Consequence Area.

The validity of the proposed model is established by a comparison between the predicted extent of the damage area and the actual extent of damage for significant gas pipeline failure incidents reported in the public domain.

Definition: The term “OSHA Recordable Injuries” is defined as Recordable work-related injuries and illnesses are those that result in one or more of the following: medical treatment beyond first aid, one or more days away from work, restricted work or transfer to another job, diagnosis of a significant injury or illness, loss of consciousness, or death. Injuries may include cases such as a cut, fracture, or sprain. Illnesses may include both acute and chronic illnesses such as a skin disease, respiratory disorder, or allergy. All needle sticks and sharps injuries involving exposure to blood or other potentially infectious materials are included.